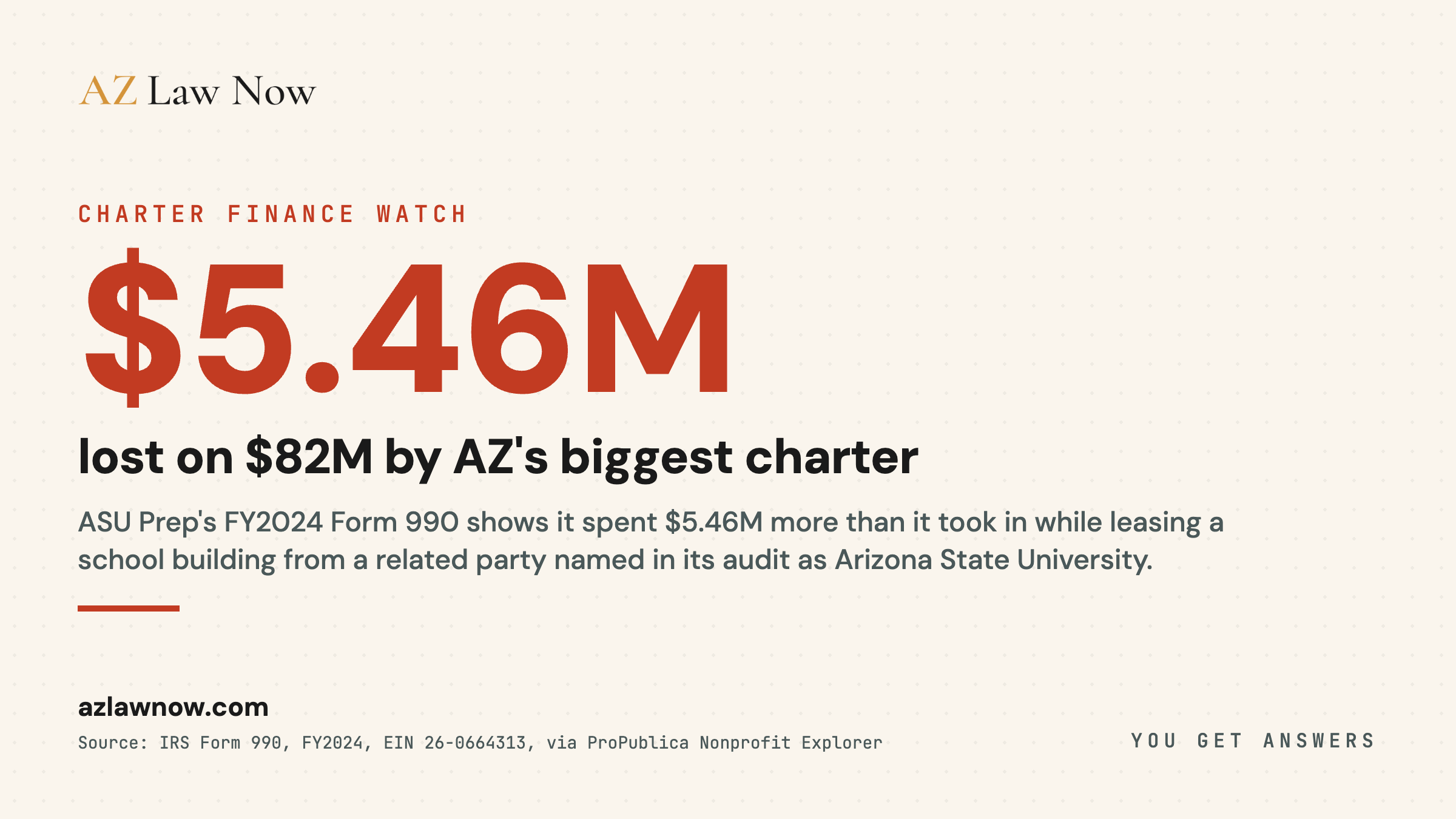

ASU Preparatory Academy is Arizona’s largest university-affiliated charter network. It’s also a separate Arizona nonprofit corporation, with its own EIN, its own board, and its own audit. Its most recent IRS Form 990, for the fiscal year ending June 2024, is publicly available through ProPublica’s Nonprofit Explorer. The headline numbers from that 990 are direct.

That’s the operating headline. The structural headline lives in the FY2021 audited consolidated financial statements, filed with the Arizona Department of Education and publicly retrievable from the ADE filing portal. Note 6 (Operating Leases) discloses, in full audit-quality language, a lease for a school-site building from a related party. The lease runs through September 2032.

The right-of-use asset is $11,543,739. Annual rent expense FY2021 was $1,404,855.

That’s not a finding. The same audit’s Schedule of Findings and Questioned Costs reports zero findings, both on the financial statement side (Section II) and on the federal award side (Section III). The auditor issued an unmodified opinion.

Related-party transactions are legal and common in nonprofit finance, provided they’re properly disclosed, board-approved, and at fair-market terms. The disclosure exists, and Note 9 names the related party: Arizona State University, the affiliated public university.

What the Audit Actually Says

The audit’s Note 6 sentence is direct: “ASU Prep leases a building used for a school site from a related party (see Note 9) under an agreement expiring September 2032, which is classified as an operating lease.”

The cross-reference to Note 9 is the standard audit pattern for putting the related-party identity into a separate disclosure. Note 9 (Related Party Transactions) is where the counterparty’s name, the relationship, and the underlying terms appear, and it identifies the related party as Arizona State University, the public university ASU Prep is affiliated with.

The same note reports $1,407,334 in affiliation fees and $3,387,252 in in-kind services from ASU during the year. The related party here is the affiliated university, not a private or founder-controlled entity.

The lease itself runs more than ten years past the FY21 reporting date. The future operating lease payments through 2026 plus thereafter total $12,479,979 nominal. Over the life of the lease through September 2032, total related-party rent commitments are a figure any responsible board would benchmark against fair-market rent for comparable Tempe-area school facilities.

The Network’s Federal-Funding Footprint

ASU Prep’s FY2021 Schedule of Expenditures of Federal Awards puts numbers on every federal dollar that flowed through the network that year. The total: $4,746,499.

The pandemic-relief lines:

Combined federal pandemic-relief expended FY2021: $2,579,590.

The non-pandemic federal lines included $1,023,860 in Title I (CFDA 84.010A), $518,767 in IDEA Special Education Grants to States (CFDA 84.027A), $184,405 combined in Charter Schools Program funds (CFDA 84.282A), and $285,859 in Summer Food Service for Children (CFDA 10.559).

Multi-year ESSER totals across FY20, FY22, FY23, and FY24 aren’t compiled in this report. The federal COVID Relief Data dashboard at covid-relief-data.ed.gov is the source of truth for the full series and is the next pull for any reader following the federal-money trail.

A related-party transaction is a transaction between an organization and someone with a position of influence over it: an officer, a director, a major donor, an entity controlled by any of those, or a family member of any of those.

The transaction itself isn’t presumptively improper. The disclosure exists so auditors, regulators, and the public can evaluate whether terms are at fair market and whether conflicts were properly handled at the board level.

The standard is in Statement on Auditing Standards 45 and the AICPA’s related-party guidance.

In nonprofit governance, the IRS Form 990 Schedule L is the parallel public-disclosure surface.

What the Public Record Will Show Next

The related party is named in the audit. Two further layers of detail sit in records that are publicly obtainable.

The first is the FY2024 audited consolidated financial statements (a year more recent than the FY21 PDF cited here). The FY24 audit will show whether the related-party lease structure persists, whether the terms changed, whether new related-party transactions were added or terminated, and whether the auditor flagged anything.

ASU Prep, as an ASBCS-sponsored charter holder, files its annual audit with the Arizona Department of Education. The filing portal is the same one used for the FY21 PDF.

The second is the lease comparables. The FY21 audit reports the rent and the related-party identity. What it doesn’t supply is the fair-market benchmark for comparable Tempe-area school facilities, against which the $1.4M FY21 rent expense can be measured. That benchmark sits in the commercial real-estate market, not in the audit.

The Statutory Frame

A.R.S. 15-181 et seq. is Arizona’s charter school statute. It defines what a charter school is, how a charter is awarded, what the sponsor’s oversight role looks like, and how a charter holder’s governing body is constituted. A.R.S. 38-503 is the state’s general public-officer conflict-of-interest statute.

The application of A.R.S. 38-503 to charter school board members rests on the public-officer determination, addressed in Arizona Attorney General opinions over the past decade.

A.R.S. 39-121 is the Arizona public-records statute. Any Arizona resident has the statutory right to inspect public records held by the Arizona Department of Education, the Arizona State Board for Charter Schools, and the charter holder itself for records relating to the expenditure of public monies.

That includes audited financial statements, board meeting minutes where related-party transactions were approved, and procurement and lease documentation.

A.R.S. 13-2310 (fraudulent schemes and artifices) and A.R.S. 44-1522 (the Arizona Consumer Fraud Act) are the felony and consumer-fraud statutes that have applied to charter-related conduct in past Arizona enforcement matters. Federal mail and wire fraud (18 U.S.C. 1341 and 1343) are the federal analogs.

None of those statutes is invoked in any public action against ASU Preparatory Academy as of this reporting date. The frame exists for accountability research, not as an allegation.

How This Differs From Founder Self-Dealing

Arizona has a documented precedent for charter related-party real estate that is very different from the ASU Prep disclosure. American Leadership Academy is the most-cited example.

Reporting by Craig Harris at The Arizona Republic documented a pattern in which entities linked to ALA founder Glenn Way bought land, built schools, and sold the school buildings back to the charter network at substantial profit, while ALA-affiliated entities collected management fees on top.

The Network for Public Education’s December 2025 Charter School Reckoning report cites that reporting in the context of national charter accountability patterns.

That pattern turns on a private, founder-controlled entity on the other side of the deal. The ASU Prep disclosure isn’t that. The FY21 audit’s Note 9 ties the related party to Arizona State University, a public university, rather than to a private real-estate entity controlled by an insider.

The ALA case is useful as a contrast: it shows what charter self-dealing looks like, and the ASU Prep audit doesn’t show that structure.

What Comes Next

Two near-term reporting moves advance this story.

The first is a public-records request to the Arizona Department of Education and the Arizona State Board for Charter Schools, under A.R.S. 39-121, for the most recent ASU Preparatory Academy audited consolidated financial statements (FY22 through FY24, the latest available).

The request also covers board meeting minutes related to the lease approval and any subsequent amendments, and ASBCS oversight correspondence with the charter holder regarding related-party transactions in that period.

The second is the comparable-rent benchmark. Tempe-area school-quality real estate has a published commercial rent market. A Costar or LoopNet pull for comparable square-footage school-use space in the relevant ZIP code yields the fair-market rent range against which the $1.4M FY21 rent expense should be measured.

For now, the disclosure is on the public record, the reported loss is on the public 990, and the audit is filed at the Arizona Department of Education. The related party is Arizona State University, the affiliated public university, and the open question is whether the rent sits at fair-market terms.

This investigation was built from the ProPublica Nonprofit Explorer 990 extract for EIN 26-0664313 and the FY2021 audited consolidated financial statements filed with the Arizona Department of Education.

Additional sources include the IRS Tax Exempt Organization Search portal, the Arizona Auditor General’s charter resources page, the Arizona State Board for Charter Schools leadership rosters, and Arizona Revised Statutes Titles 15, 38, and 39.

If you have the FY22 through FY24 ASU Preparatory Academy audits, lease comparables for the related-party rent, ASBCS sponsor file correspondence, or board meeting minutes referencing the lease approval, contact AZ Law Now.

We report from primary sources and protect the identity of sources who share information.

Frequently asked questions

What is ASU Preparatory Academy and how is it related to Arizona State University?

What are the FY2024 financials per the IRS Form 990?

What does the FY2021 audit say about a related-party lease?

Did the FY2021 audit identify any findings or compliance problems?

How much federal pandemic-relief money did ASU Prep receive?

Has ASU Prep faced any state or federal enforcement action since 2020?

Why does this story matter to Arizona families with charter-school children?

What is the controversy with charter schools?

Who oversees charter schools in Arizona?

How to report fraud in AZ?

What are some criticisms of charter schools?

Sources & references

- ProPublica Nonprofit Explorer. (2026). ASU Preparatory Academy, EIN 26-0664313, FY2024 IRS Form 990 extract. Retrieved May 1, 2026, from https://projects.propublica.org/nonprofits/organizations/260664313

- ASU Preparatory Academy. (2021). Consolidated Financial Statements, Year Ended June 30, 2021, including Schedule of Expenditures of Federal Awards and Schedule of Findings and Questioned Costs. Filed with the Arizona Department of Education. Retrieved from https://www.ade.az.gov/sfsinbound/GeneralUpload/183788.pdf

- Internal Revenue Service. Tax Exempt Organization Search. Retrieved from https://www.irs.gov/charities-non-profits/tax-exempt-organization-search

- Cause IQ. ASU Preparatory Academy organization profile. Retrieved from https://www.causeiq.com/organizations/asu-preparatory-academy,260664313/

- Charity Navigator. ASU Preparatory Academy rating profile. Retrieved from https://www.charitynavigator.org/ein/260664313

- Arizona Auditor General. Charter Schools resources page. Retrieved from https://www.azauditor.gov/resources/charter-schools

- Arizona State Board for Charter Schools. Board members and current leadership. Retrieved from https://asbcs.az.gov/leadership-category/board-members

- Arizona State Directory. Board for Charter Schools staff listing. Retrieved from https://azdirect.az.gov/board-charter-schools

- Arizona Revised Statutes Title 15, Chapter 1, Article 8 (Charter schools). Retrieved from https://www.azleg.gov/arsDetail/?title=15

- Arizona Revised Statutes 38-503 (conflict of interest, public officers and employees). Retrieved from https://www.azleg.gov/ars/38/00503.htm

- Arizona Revised Statutes 39-121 (public records inspection). Retrieved from https://www.azleg.gov/ars/39/00121.htm

- U.S. Department of Education. COVID Relief Data dashboard, Arizona state profile. Retrieved from https://covid-relief-data.ed.gov/profile/state/AZ

- Network for Public Education. (2025, December). Charter School Reckoning: Disillusionment report (referenced for context on related-party real-estate patterns in U.S. charter schools, citing Craig Harris reporting on American Leadership Academy in The Arizona Republic). Retrieved from https://networkforpubliceducation.org/wp-content/uploads/2025/12/Charter-School-Reckoning-Disillusionment.pdf

- Arizona Department of Education. Equalization Assistance schedules and per-pupil basic state aid. Retrieved from https://www.azed.gov/finance/fy-2026-monthly-payment-and-azeds-processing-schedule